Subscription Fees Will Change the Client Experience—Whether You Want Them to Or Not

Search

Subscribe

Companies like Apple, Google, and Amazon have long been the boogeymen of financial services. They collectively form the spectre haunting wealth management, you might say.

Everyone wants to know when they’re going to make their entry into the space and take over for the everyman advisor, who won’t be able to compete with their scale and the long-term customer trust they’ve built over the years.

And on March 25th, Apple announced the Apple Card and made its first foray into personal finance. But while the new credit card seems to have enticed Apple fanboys, its bonuses didn’t do much to grab the attention of financial pundits.

Soon after, Schwab announced a new subscription model for its Intelligent Portfolios. For a low price, you get a financial plan for a set fee and pay a monthly subscription after that for portfolio management.

The Schwab announcement has done more to shake things up in the industry, but taken together both of these moves show the way forward for consumers and advisors. And while consumers are becoming more empowered, advisors are going to become more challenged.

Put simply, consumer demands are about to go way up.

The difference, though, isn’t about fees—which is where many are missing the mark. As an advisor, you aren’t competing directly with Apple for clients right now, and while there may be some overlap with Schwab Intelligent Portfolios, it’s also not a heavy segment.

What you are competing with them on are the expectations for what a client experience should look and feel like.

Consumers are more willing to pay for financial advice now than in past years, but why should an investor with a $2 million portfolio receive a worse client experience than someone with $3,000 invested with Schwab?

Schwab’s subscribers are typically between 25-44 years old with incomes of $50,000 to $100,000 a year. This is an underserved market for advisory firms. If this group’s first experience with wealth management is with Schwab through subscription fees, then 15 years from now when they’re ready to move up and begin working with a traditional advisor, then their entire perception of working with an advisor will be informed by that relationship.

I think that we are about to experience a generational shift in how people expect to receive and pay for financial advice, largely due to the introduction of subscription fees by such a major player. In every industry in which subscription services have been introduced, that industry has been turned on its head in short order.

[Of course, it bears highlighting that subscription or retainer fees aren’t entirely new in wealth management. The folks at XY Planning have been doing the Lord’s work in pushing this idea forward for some time. The difference is that now the model is being taken up by major, nationwide players who can enact a true shift in widespread attention toward the structure.]

Let’s take a look at a few of the other instances where subscription disruption has occurred to see what we might expect to happen next in financial services.

Microsoft Office

Microsoft probably isn’t the first company you think of when you think about game-changing subscription models, but they’ve transformed how people access their Microsoft Office products in a few short years.

I’m old enough to remember when you had to take out a small additional student loan at the university bookstore to purchase a reduced price copy of the Microsoft Office suite.

But a little over a handful of years ago, Microsoft began driving consumers away from purchasing the Office suite as a standalone product with Office 365, a subscription service.

Office 365 offered advantages over the traditional Office product, including more device support and access to files across devices.

In late 2017, Microsoft had 120 million active monthly subscribers to Office 365 and revenue from subscriptions had overtaken standalone purchases. Office 365 launched only six years before that.

Spotify and Apple Music

Example number two: Streaming music instead of buying albums.

While the music purists out there might groan about it (“you’ve got to play the entire album through from start to finish to get the full experience”) streaming is now the primary way to engage with musical artists.

Again, the turnover happened rapidly.

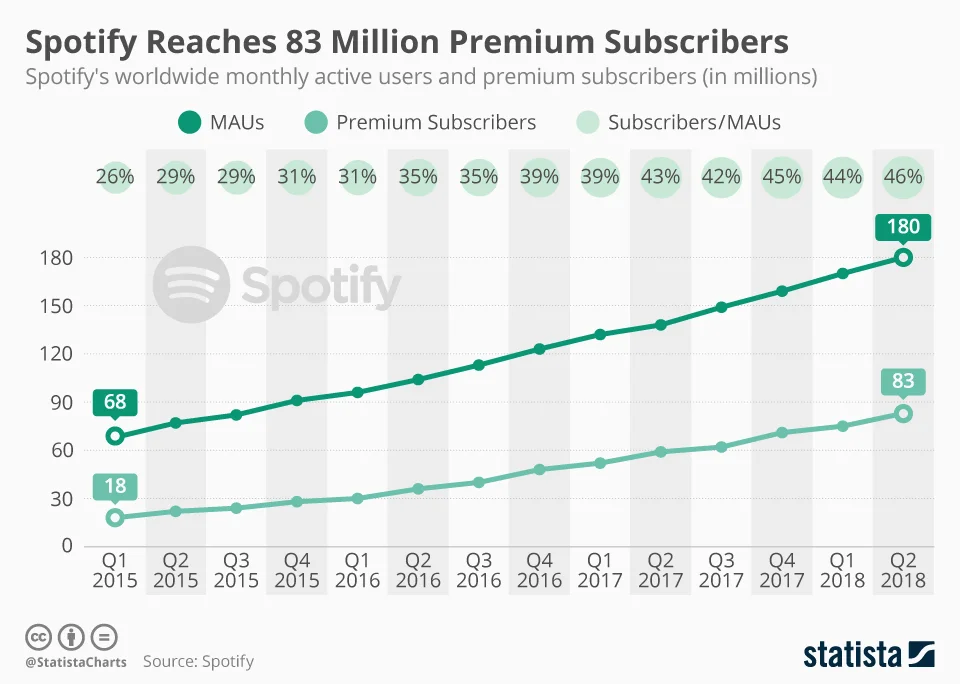

Spotify (who many consider the current leader in streaming music) entered the United States market in 2008. In late 2018, streaming accounted for 75% of music revenue. Digital sales followed it up with 12% of the total and physical purchases came next at only 10 percent.

In only three years, Spotify went from 68 million worldwide users to over 180 million.

But perhaps most impressive of all is that streaming music is increasing the total music spend for consumers. Streaming jumped 34% to almost $9 billion in revenue, and makes up 47% of all the world’s revenue for recorded music now.

Notably, streaming is still just getting started. Apple joined the movement with Apple Music and just recently surpassed Spotify for the lead in paid US subscribers.

Netflix

Once upon a time, we went to a video store called Blockbuster to rent movies. Then a company came along that shipped DVDs to you in the mail. That seems almost quaint now.

But then they started streaming movies to your TV, instantly. And the rest is history.

It’s probably the most well-known example of how streaming has disrupted traditional industries, so you already know the story of how Netflix has revolutionized TV and movies. We won’t get into it here—but don’t forget about the rapid change it introduced.

How Apple Changes the Conversation

So, how does Apple’s credit card play into all this?

It’s not a stretch to say that on-boarding is still the worst part of the client experience for wealth management firms—even with the advancements made by some custodians with digital new account opening.

Consumers expect mobile-friendly, all-digital solutions because that is what they are getting in every other service they receive.

And unfortunately, advisors are a long way from meeting shifting consumer expectations. In Financial Planning’s recent tech survey, the results show that leading digital tools like form-filling solutions and robo-advisor usage are still struggling to find mass adoption among firms.

And this is how Apple will change consumer expectations for what it’s like to work with a financial services company.

The Apple credit card signup process all takes place on your phone, and it’s all instantaneous. It’s an improvement on the digital sign-up experience that robo-advisors have provided.

You launch an app on your iPhone, fill in your info, get approved, and your card is loaded and ready to use on your iPhone immediately. The process promises to be 100% digital and the true definition of seamless.

You are not competing with Apple for clients directly, but you will soon be competing against the expectations for what a financial experience should look and feel like when clients come to you having already experienced that kind of “Apple magic.”

Subscription Fees Address a Weakness in Financial Advice

Subscription fees get at one of the financial services industry’s weak points: transparency.

Most RIA firms believe themselves to be transparent. They think they’re fiduciaries, and by most accounts they follow the laws about disclosures and avoid conflicts of interest.

But following fiduciary rules doesn’t automatically equate to transparency. How many advisors show their fee structure on their website? The argument that “no one else is doing it” isn’t good enough anymore.

Telling someone the percentage that they’ll pay you is better, but still doesn’t equal full transparency. How many advisors take the time to have this type of conversation:

“You fall into our 1.25% fee bracket. That means that if your investment accounts with us total $300,000 and don’t fluctuate at all over the course of the year up or down, you’ll pay us $3,750 over the course of the year.”

There aren’t many advisors who take that next step and talk in terms of actual dollars. Usually it falls to the client to figure out those calculations for themselves.

And let’s not get started in how fees are withdrawn. Most advisors don’t send separate invoices to clients; instead, the fees are shown on a dozen-page statement along with an avalanche of other information about a portfolio.

Fees are easily hidden, even in a seemingly transparent process.

A subscription fee doesn’t let an advisor hide any of that. The amount that a client pays for financial advice is up front and known from the start.

Additionally, a subscription fee forces advisors to think more completely about their service offerings and the value they provide.

People like me, who get almost everything via subscription, are accustomed to arriving at a check-out page and seeing a checklist of all that’s being provided as part of the subscription.

For Netflix, it may be a checklist that shows how many screens can be used at once, the total number of account users, the quality of the streaming video, and the price.

If you had to present the services you offer in a simple checklist like this, along with the price you would charge each month, could you do it? Yes, you could pull the Services you have listed in your Form ADV, but it needs to be as simple and understandable as the Netflix model (you get to watch one screen at once, or four at once).

The Big Question About Subscription Fees for Financial Advice

In these other industries, a subscription fee makes sense because it is clear that you are getting more from it.

You may have rented a single movie from Blockbuster for $2.99, but subscribing to Netflix cost you $10 a month and includes the ability to watch an unlimited amount of movies (so long as they’re on the service already).

That 3x price increase makes sense when you compare “unlimited” viewing to “single use” viewing. The value is clear.

You can buy a single album for $10, or you can subscribe to Spotify for $10 a month and get that album, plus every other recording your favorite band has released (live albums included) and almost every other recording you could possibly want.

Again, the value of the subscription model is clear, even if you do end up paying more in the end.

For financial advisors, the value conversation is murkier. An AUM fee already includes unlimited advice and the entirety of services an advisor can offer. A client who calls their advisor twice a month doesn’t receive any overage alerts, versus a client who only calls their advisor twice a year.

Advisors are already offering the Ultimate 4K Streaming Package as the ordinary service.

A subscription fee versus AUM fee conversation necessitates that you are able to put together a tangible comparison of why the subscription fee makes more sense, and how the client gets more value out of it in the end.

It’s important at this point to understand that subscription fees don’t have to be bottom of the barrell. You don’t have to match what Schwab offers. Think of it as the “family subscription” tier—you get more, so you pay more.

Look at this way. If you have a client with a $300,000 portfolio and you currently charge 1% of AUM, your revenue on that client is $3,000 for the year.

In a subscription model, you could instead charge a $600 flat fee for a financial plan (the average standalone cost is $2,400) and then have a monthly subscription of $200 per month for ongoing advice. At the end of the year, you’re still making $3,000 in revenue.

The difference, of course, is that the feeling is much different for the consumer. You’re no longer sliding money out of their account each quarter; they are actively engaging your services.

Subscription fees put the power in the hands of the consumer, not the company providing the service.

The bigger question to ask yourself is can you price a subscription at $200/month? The market will decide that—but you have to prove that your value is 6.5x higher than what a client can get from Schwab.

The future of your business may end up resting not only on whether you can substantiate why you charge what you do, but also explain the method behind how you bill.

Looking for someone to help you refresh your marketing strategy, write a new website, or speak at your next event? Click here to get in touch.

Featured Image: Photo by Aneta Pawlik on Unsplash